When buying a home in the U.S., you will almost certainly hear the term mortgage underwriting. You may have submitted your loan application, but questions remain: Is my documentation sufficient? When will I be approved? What exactly does the lender review?

In this article, we clearly explain what mortgage underwriting is, how the U.S. home loan approval process works, and what Korean buyers should prepare in advance.

What Is Mortgage Underwriting?

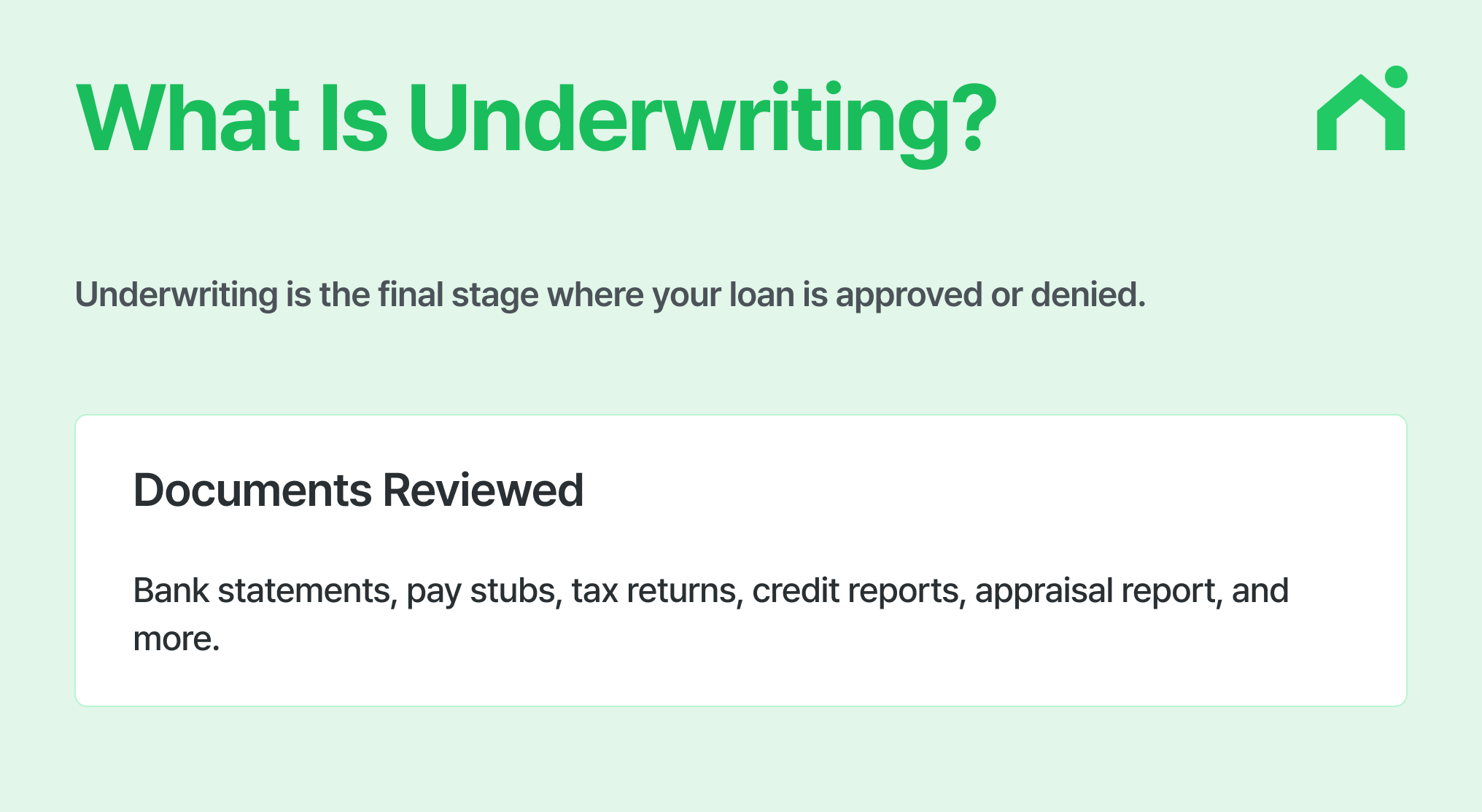

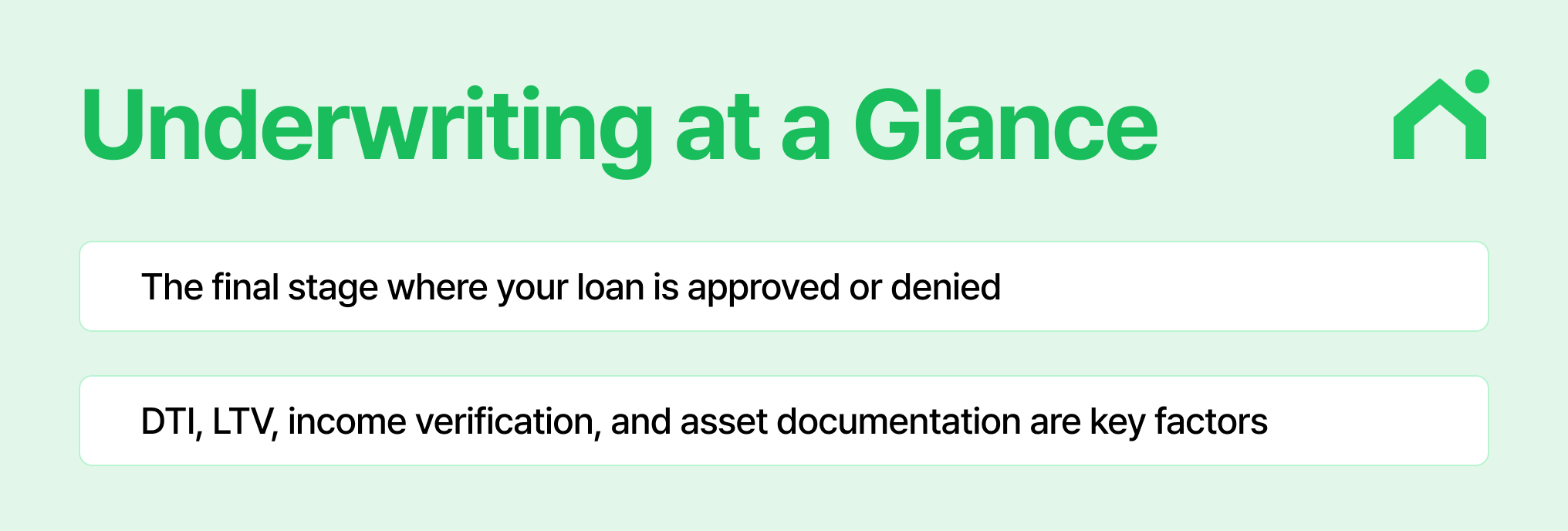

Mortgage underwriting is the process where a lender carefully reviews a borrower’s income, assets, debts, credit history, and property details to determine whether the loan should be approved.

The lender verifies the information on your application against actual documentation such as:

- Bank statements

- Pay stubs

- Tax returns

- Credit reports

- Property appraisal reports

How Do Underwriters Evaluate a Loan?

Underwriters typically assess loans using the “5 C’s.” In simple terms, they evaluate two main questions:

- Is the property worth the price?

- Can the borrower realistically afford the payments?

| Category | Meaning | Example Documents |

|---|---|---|

| Credit | Credit score, payment history | Credit report |

| Capacity | Debt-to-income ratio (DTI), income stability | Pay stubs, W-2s, tax returns, employment verification |

| Capital | Down payment, closing costs, reserves | Bank statements, investment account statements |

| Collateral | Property value relative to loan amount | Appraisal report |

| Character/Conditions | Occupancy type, market conditions, loan program rules | Purchase agreement, lease agreement (if applicable) |

What Is the U.S. Mortgage Underwriting Process?

1. Loan Application & Pre-Approval

You submit basic income, debt, and asset information. The system provides an initial estimate of eligibility.

2. Formal Application & Document Submission

You typically submit:

- Two years of tax returns

- Pay stubs

- Bank statements

- ID and residency documents

- Purchase agreement

3. Automated Underwriting (AUS) + Manual Review

The automated system evaluates DTI, LTV, and credit first.

Then an underwriter reviews any exceptions or complex income situations (self-employment, overseas income, etc.).

4. Conditional Approval

Most approvals come with conditions such as:

- Additional bank statements

- Updated employment verification

5. Clear to Close

Once all conditions are satisfied, final approval is issued and the closing process begins.

What Are DTI and LTV?

DTI (Debt-to-Income Ratio)

The percentage of your monthly income used to pay debts.

LTV (Loan-to-Value Ratio)

The loan amount compared to the home’s value.

- Formula:

LTV = (Loan Amount ÷ Lower of Purchase Price or Appraised Value) × 100

How Should Korean Buyers Prepare for Mortgage Underwriting?

For Korean or foreign borrowers, proving repayment ability and documenting down payment sources are critical.

1. Income Documentation

If earning income in the U.S.:

- W-2s

- Pay stubs

- Tax returns (usually two years)

If self-employed:

- Business tax returns

- Profit & Loss statements

If using Korean income:

- Korean income certificates

- Payroll records

- Tax withholding documents

(Translation and notarization may be required.)

2. Asset & Down Payment Documentation

- Bank statements (usually most recent two months)

- Investment account statements

- Proof of down payment source

- Gift documentation (if applicable)

Lenders may also review reserves — funds available to cover several months of mortgage payments after closing.

3. Debt & Credit

- U.S. credit report

- Korean credit or debt may not directly apply, but lenders may consider overall financial obligations.

Transparency with your lender is essential.

4. Property Documentation

- Signed Purchase Agreement

- Appraisal ordered through the lender

Frequently Asked Questions

Q1. How long does mortgage underwriting take?

The entire mortgage approval process, including underwriting, typically takes 40–50 days. Timelines vary depending on documentation and loan program.

Q2. What is conditional approval?

It means the loan is likely approved pending submission of additional documents.

Q3. Will high DTI automatically cause denial?

Not necessarily. Strong income, sufficient reserves, or a low LTV can sometimes offset a higher DTI.

Q4. Can I qualify using only foreign income?

Certain programs (such as Foreign National loans) allow foreign income, but documentation standards vary by lender.

Mortgage Underwriting at a Glance

Check Your Mortgage Eligibility with Loaning.ai

Mortgage underwriting approval depends on your financial profile.

Consult with a Korean-speaking advisor at Loaning.ai to determine which mortgage options fit your income and assets—and what you need to prepare to pass underwriting successfully.