What It Is and What It Covers

A Rate Lock is a tool that protects your mortgage interest rate during the period between loan application and closing. When you apply for a mortgage to buy a home, there is typically a period of several weeks — sometimes close to two months — between your application and closing. During this time, market interest rates may rise, or lender terms may change.

If rates increase before you close, your expected monthly payment could rise. A Rate Lock reduces this uncertainty by securing your interest rate and certain loan terms for a specified period.

Why This Step Matters Before Closing

At this stage of the transaction, protecting your loan terms becomes critical.

The lock period you choose — and whether extensions or float-down options are available — can impact your monthly payment and total interest cost for years.

Choosing the right timing and duration is not just a technical decision. It directly affects your long-term cash flow.

At the time of application, the payment may have seemed affordable. However, if interest rates spike between underwriting and closing, your monthly payment can increase — even for the same home and loan amount.

✅ Having to Reconsider Your Budget or Home Choice

If rates rise, both your total interest cost and DTI ratio increase. You may need to restructure your down payment, adjust the home price, or even search for a more affordable property.

✅ Unnecessary Extension Fees and Costs

If you choose a lock period without careful planning and closing is delayed, multiple extensions can end up costing more than selecting a slightly longer lock from the start.

✅ Missing Opportunities During a Rate Decline

If you fail to use a float-down option or adjust your lock timing, you may miss the chance to secure a lower interest rate.

Understanding It Within the Home Buying Timeline

Based on the actual home-buying process, let’s review when Rate Lock typically comes into play.

In summary, this strategy helps align your interest rate with your closing timeline.

| Mortgage Process | Detail |

|---|---|

| Pre-Approval | • This is the stage where you confirm an estimated approval amount and potential interest rate. • Because a specific home and closing date are usually not finalized yet, Rate Lock is not commonly applied at this stage. |

| Offer Submission & Acceptance | • Once you choose a home and the seller accepts your offer, the purchase agreement typically includes an estimated closing date. • From this point, discussions begin about when to lock the rate and how many days of lock are needed. |

| Inspection · Appraisal · Underwriting | • Property inspection, appraisal, and underwriting review proceed simultaneously. • Since document revisions or additional verifications may delay the timeline, these variables must be considered when determining the lock period. |

| Closing Stage | • If closing is completed within the lock period, the agreed interest rate, points, and certain fee conditions are applied to the loan. • If closing occurs after the lock expiration date, you may face an Extension or Re-Lock situation. |

Understanding the Lock Structure and Cost

While specific options vary by lender, Rate Lock periods are generally structured as follows.

The key is to consider “expected closing date + potential delays” together and choose a period that is neither too tight nor unnecessarily long.

| Lock Period | Cost Considerations |

|---|---|

| 30-Day Lock | · Used when closing is expected quickly · Because the period is shorter, additional fees or rate premiums are typically lower |

| 45-Day Lock | · Often selected to allow reasonable flexibility for inspection, appraisal, and underwriting · A common balance between “safety margin + cost” |

| 60-Day or Longer Lock | · Used when the timeline may extend due to new construction, possible construction delays, or complex documentation · A premium may apply in the form of points or a slightly higher rate |

What If the Lock Period Isn’t Long Enough? Extension Options

Unexpected changes occur more often than people think in home transactions.

Inspection results may require renegotiation.

The appraisal schedule may be delayed.

The seller’s circumstances may push closing to a later date.

If you cannot close before the lock expires, you may request an Extension from your lender.

However, if you initially choose a lock period that is too short and end up extending multiple times, the total cost may exceed what you would have paid by selecting a slightly longer lock period from the start.

Key Concepts to Understand Alongside Rate Lock

To see the bigger picture, Rate Lock should be understood together with other core mortgage concepts. Reviewing the concepts below will help you build a more informed locking strategy.

| Concept | Meaning | Relationship to Rate Lock |

|---|---|---|

| Interest Rate | The base interest rate applied to your loan | This is what a Rate Lock actually “locks.” The interest rate remains fixed during the lock period. |

| APR | The interest rate plus fees, expressed as an annual cost | When locking a rate, you should compare not only the interest rate but also the APR to understand the total cost structure. |

| DTI (Debt-to-Income Ratio) | The ratio of your debt payments compared to your income | If interest rates rise, DTI increases even with the same loan amount. A Rate Lock helps make your DTI more predictable. |

| PITIA | Principal + Interest + Taxes + Insurance + HOA + other costs (total monthly housing payment) | Rate Lock mainly affects the “P (Principal) + I (Interest)” portion. You should evaluate the full PITIA structure to assess your true monthly burden. |

| Closing Timeline | The schedule from offer, inspection, appraisal, underwriting, to closing | This must be considered when choosing an appropriate lock period. |

Ask About the Right Time to Lock Your Rate

At Loaning.ai, you can chat with us to find out when it’s best to lock your rate.

If you have any mortgage-related questions, feel free to ask—no personal information required.

Frequently Asked Questions (FAQ)

Q1. If I choose a Rate Lock, is my interest rate completely fixed?

If you complete closing within the lock period, the agreed interest rate, points, and certain fee terms are generally honored. However, if you change the loan structure or if your financial situation (income, assets, debts, etc.) changes significantly, the lender may need to re-evaluate the terms. It’s important to confirm in advance under what conditions the lock remains valid and when it may be re-priced.

Q2. Are there disadvantages if I cancel a Rate Lock later?

If you break the lock or move to another lender, fees may apply, and it may be difficult to receive the exact same terms again from the original lender. If you want to compare multiple lenders, many borrowers compare quotes during the Pre-Approval stage, select the final lender, and then proceed with the Rate Lock.

What Is Rate Lock? A Quick Summary

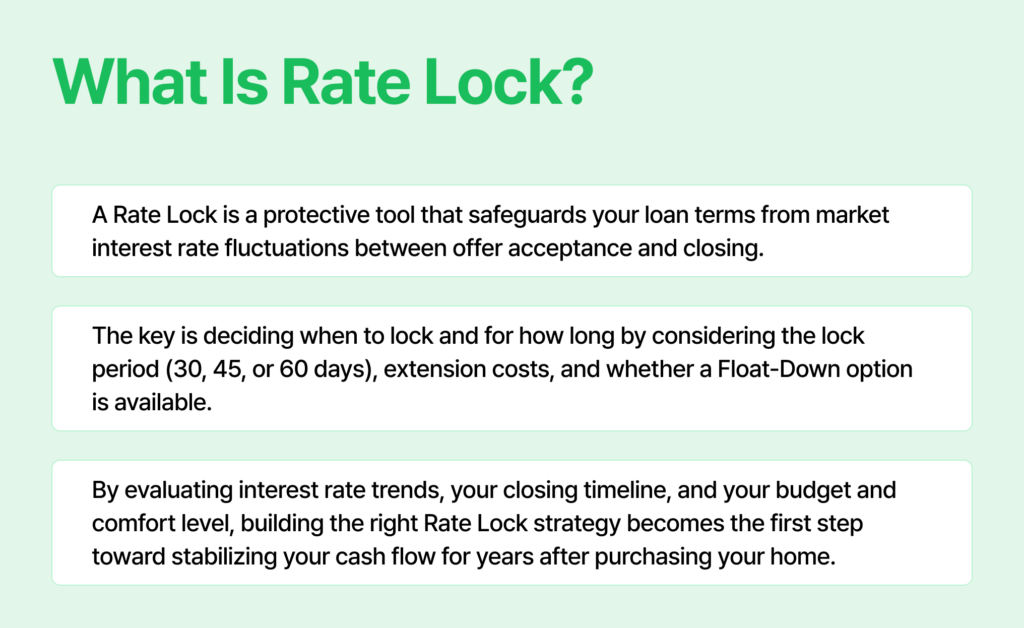

- A Rate Lock is a protective tool that safeguards your loan terms from market interest rate fluctuations between offer acceptance and closing.

- The key is deciding when to lock and for how long by considering the lock period (30, 45, or 60 days), extension costs, and whether a Float-Down option is available.

- By evaluating interest rate trends, your closing timeline, and your budget and comfort level, building the right Rate Lock strategy becomes the first step toward stabilizing your cash flow for years after purchasing your home.