Mortgage DTI Q&A

A prospective homebuyer recently reached out to Loaning.ai with questions about mortgage DTI while searching for their first home near Los Angeles. Though they had steady annual income, they were concerned about existing loan balances and how those debts might affect mortgage approval.

Using this case as an example, let’s break down what DTI is, how it’s calculated, and why it matters for your mortgage application.

.

What Is DTI?

Mortgage DTI (Debt-to-Income Ratio) is the percentage of your gross monthly income that goes toward paying monthly debt obligations. Lenders use mortgage DTI to evaluate a borrower’s ability to repay a home loan. In general, the lower your DTI, the higher your chances of approval — and the more favorable your loan terms may be.

How Is DTI Calculated?

Mortgage DTI is one of the most important financial indicators reviewed during the mortgage application process. It shows lenders how much of your income is already committed to debt payments.

If your DTI is high, it signals greater financial risk, which may lead to:

- Loan denial

- A reduced loan amount

- A higher interest rate

DTI Formula

DTI (%) = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

What Counts as Monthly Debt?

- Proposed monthly mortgage payment (including the new loan)

- Auto loans

- Student loans

- Minimum credit card payments

- Personal loans and other recurring debt

.

Calculation Example

If your gross monthly income is $7,000, and:

- Monthly mortgage payment: $2,000

- Other monthly debts (auto loan, student loans, etc.): $500

Your total monthly debt is $2,500.

DTI = ($2,500 ÷ $7,000) × 100 = 35.7%

.

Approval Guidelines and Ranges

| DTI Ratio | Category | Interpretation |

|---|---|---|

| 36% or below | Excellent | Strong approval likelihood, favorable loan terms |

| 37–43% | Acceptable | Most loans approved, depending on lender guidelines |

| 44–50% | Limited | Approval possible but may involve higher rates |

| Above 50% | High Risk | Approval unlikely without compensating factors |

Mortgage DTI Limits by Loan Type

| Loan Type | Recommended DTI | Features |

|---|---|---|

| Conventional Loan | Up to 43% | Standard underwriting guideline |

| FHA Loan | Up to 50% | Government-backed, more flexible for lower credit |

| Foreign National Loan | 35–43% | Designed for non-U.S. borrowers, foreign income accepted |

Approval ultimately depends on your credit score, assets, and overall financial profile.

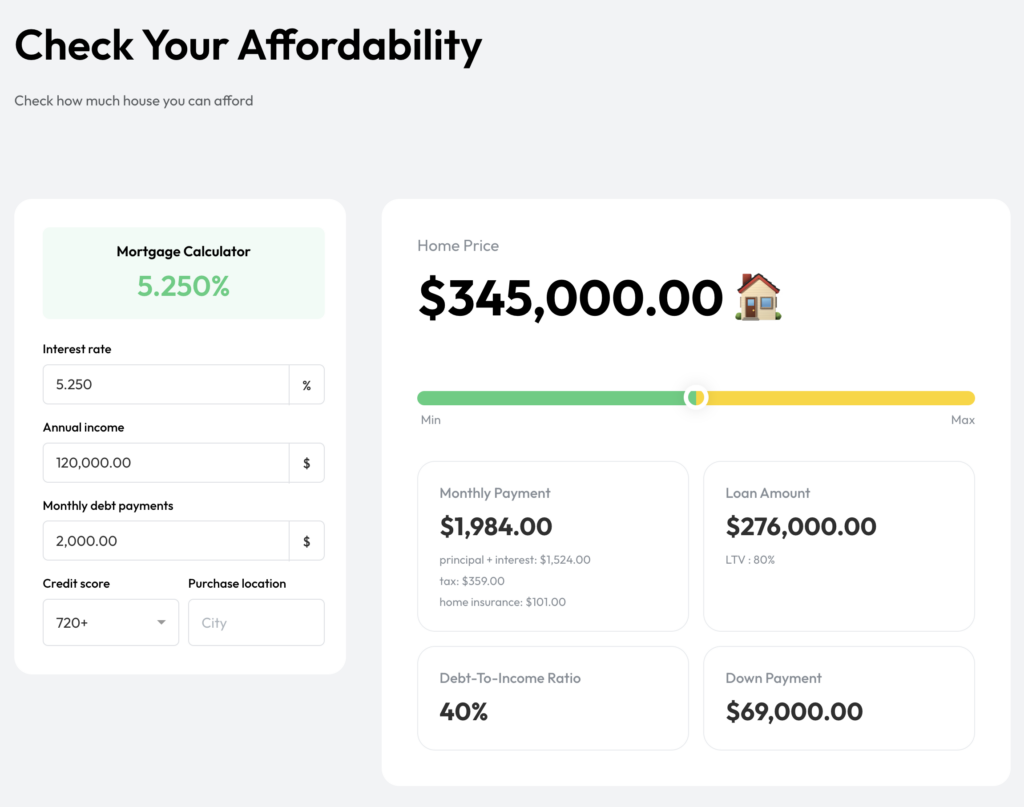

How to Calculate Mortgage DTI Easily

With Loaning.ai, you can enter your annual income, debts, credit score, and target city to estimate:

- Mortgage DTI

- Loan eligibility

- Maximum borrowing amount

- Estimated monthly payment

- Required down payment

You can compare loan options based on current market rates and your financial profile — all in one place.

※ The case example in this article is hypothetical and for illustrative purposes only—it does not represent an actual client. Actual loan amounts, rates, and approval depend on individual credit, income, debt, assets, loan type, and market conditions.

※ Estimate only—not a loan commitment. Assumptions: U.S. citizen, 2+ years of tax returns, full documentation, single-family primary residence, FICO 740, LTV 70%, property tax 1.25%, homeowners insurance 0.250%, 20% down (no PMI). Does not guarantee approval or denial.

Click the green button below to estimate your mortgage DTI and loan limit.

Other Key Metrics to Review

| Term | Description |

|---|---|

| LTV (Loan-to-Value) | Loan amount relative to property value — lower is generally safer |

| Credit Score | Indicator of borrower creditworthiness |

| Asset Documentation | Proof of funds and income required for underwriting |

DTI works together with these metrics to determine final approval.

Tips for Managing Your Mortgage DTI

Lowering and maintaining a healthy mortgage DTI improves your approval chances. Consider the following:

- Pay down high-interest debt first

- Avoid new loans before and during the application process

- Increase documented income when possible

- Provide accurate financial documentation

- Use Loaning.ai’s DTI calculator to evaluate loan scenarios before applying

Frequently Asked Questions (FAQ)

Q1. When is DTI calculated?

Mortgage DTI is calculated during pre-approval, formal application, and final underwriting. Lenders verify income and debt documentation at each stage.

Q2. Does a high DTI automatically mean denial?

Not necessarily. Strong assets, a larger down payment, or compensating factors may offset a higher DTI.

Q3. What is the typical approved DTI range?

Most approvals fall between 36% and 43%, though FHA loans may allow up to 50%.

Q4. How can I lower my DTI?

You can reduce debt, increase income, add a co-borrower, or increase your down payment.

Q5. What else affects mortgage approval besides DTI?

LTV, credit score, employment stability, and asset reserves are also considered.

Mortgage DTI: Quick Summary

DTI (Debt-to-Income Ratio) measures the percentage of your monthly income that goes toward debt payments. It directly impacts both mortgage approval and loan amounts—most lenders prefer a DTI of 43% or below. A lower DTI improves your approval chances, while a higher DTI suggests heavier debt burden and may reduce approval likelihood. Keeping your DTI low is essential for securing favorable mortgage terms.

If you’d like to better understand your DTI or explore your borrowing options, use Loaning.ai to calculate your DTI and compare mortgage scenarios before applying.