📝 Loan Application & Initial LE: 3-Line Summary

- This stage marks the beginning of your official mortgage application and the first moment you see your loan terms expressed in real numbers.

- The lender issues the Initial Loan Estimate (Initial LE), and you formally confirm your intent to proceed by signing the Intent to Proceed (ITP).

- By preparing documents correctly, reviewing the LE, and signing the ITP at the right time, you can significantly speed up underwriting, appraisal, and closing.

Once you understand the three key points of the Loan Application & Initial LE stage, plus the “Zero Fee Rule,” this step becomes much less intimidating. Today, we’ll explain how to pass the document review on the first try and how to time your ITP signature to protect your money.

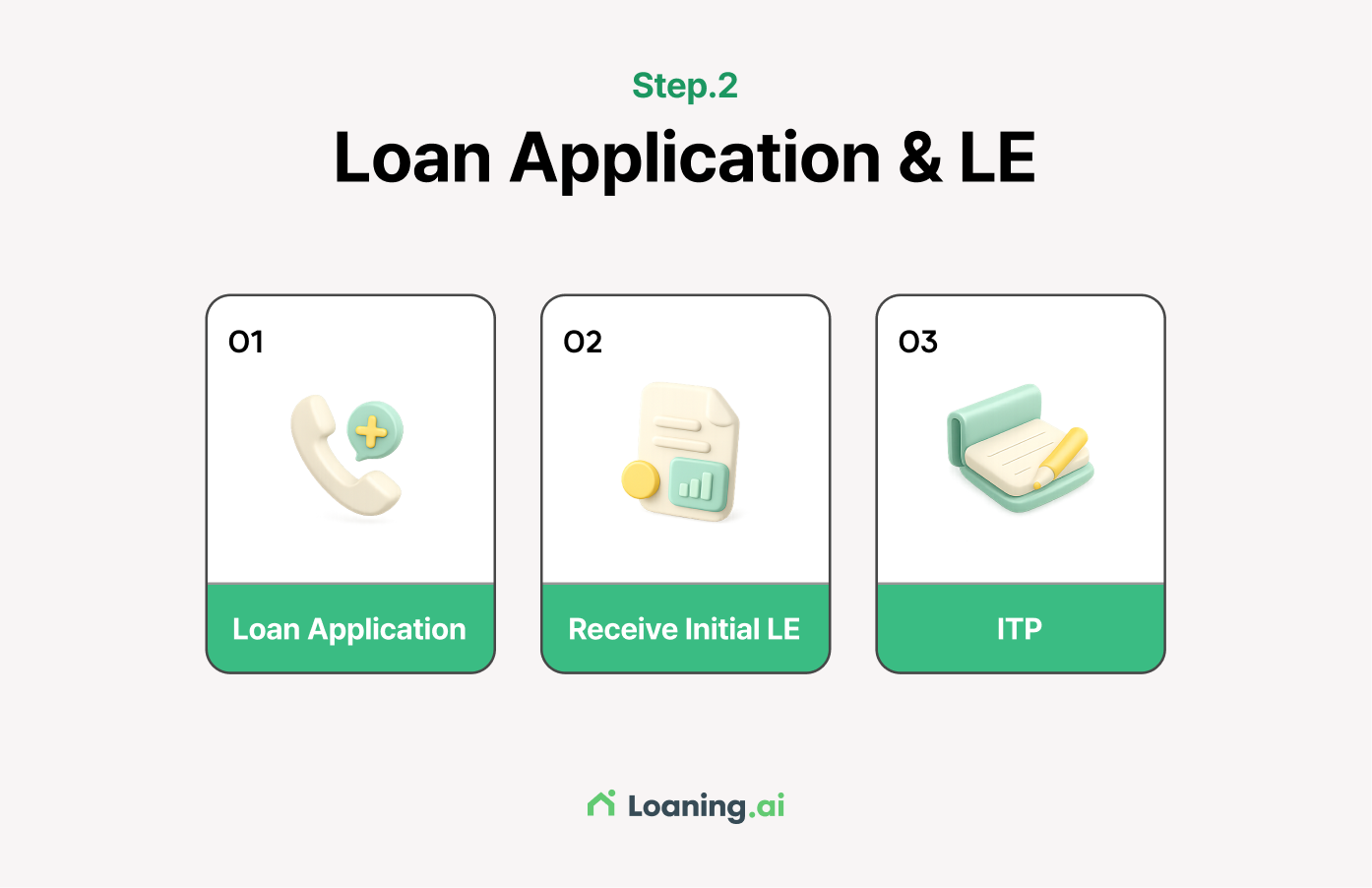

1. Loan Application & Initial LE: The Beginning of Your Official Application

This stage may look complicated, but you really only need to remember three steps: Application → Initial Loan Estimate (LE) → Intent to Proceed (ITP).

✅ 3-Step Process

| Step | Description |

|---|---|

| Application | You officially submit your income, assets, identification, debts, and property information to the lender. |

| Initial LE | You receive the Initial Loan Estimate, which outlines your preliminary loan terms and costs. |

| ITP | If you agree with the estimate, you sign the ITP to move forward. |

2. Required Documents

If your documents keep getting rejected, the issue is usually the format, not the content. Be sure to check the tips below.

[1] Required for All Borrowers

| Document | Type | Purpose |

|---|---|---|

| Government ID SSN Verification Green Card/Visa (if applicable) | Identification | Verifies the borrower’s identity. |

| Purchase Agreement | Real Estate Contract | Confirms which property the borrower is buying and at what price. |

| Bank Statements | Bank Transaction Records | Last 2 months. Verifies funds for the earnest money and down payment. |

| Credit Report | Credit Check | Assesses the borrower’s eligibility for a mortgage. (Consent needed) |

| Borrower Certification | Consent Form | Confirms the borrower’s consent for credit checks and income/asset verification. |

| EMD Receipt | Proof of Funds | Verifies the EMD and activates the contract. |

② Submit all pages of the past 2 months of statements, even blank pages (e.g., if it says “1 of 5,” you must upload all 5).

[2] For a W-2 employee

| Document | Type | Purpose |

|---|---|---|

| Pay Stubs | Payroll Statements | Last 30 days. Verifies income stability and helps determine loan eligibility/amount. |

| Form W-2 or Tax Return | Annual Income Report | Last 2 years. Checks credit score and debt-to-income ratio (DTI). |

| Verification of Employment (VOE) | Employment Verification | Confirms current employment status when required. |

[3] For a Self-Employed/Business Owner

| Document | Applicable To | Purpose |

|---|---|---|

| Schedule C (Form 1040) | Sole Proprietor | Last 2 years. Verifies personal business income and freelance income. |

| Business Tax Return | Corporation/Partnership Owners | Last 2 years. Confirms the financial status of the corporation or partnership. |

| Schedule K-1 | Shareholders/Partners | Last 2 years. Shows the portion of business income allocated to the borrower. |

| Profit & Loss Statement (P&L) | Self-Employed | Shows year-to-date business income after the most recent tax filing. |

3. Initial Loan Estimate (LE): What to Look For

After your application is submitted, the lender must send the Initial LE within 3 business days, per U.S. TRID regulations. The Initial LE is exactly what it sounds like—a preliminary estimate. It includes:

❷ Monthly Payment (Principal & interest, plus property tax and homeowners insurance if applicable)

❸ Estimated Closing Costs (Lender fees, title/escrow fees, government fees, etc.)

❹ Basic Loan Structure (Fixed vs. adjustable rate, 30-year vs. 15-year term, etc.)

Under TRID, lenders cannot charge you any fees before you: receive the Initial LE, and sign the ITP.

4. What the ITP (Intent to Proceed) Means

After reviewing your Initial LE, you must sign the ITP to officially authorize the lender to begin third-party work such as appraisal and title. If you want a faster closing, signing the ITP promptly is essential.

Without the ITP, the lender cannot order the appraisal or initiate third-party verifications, which delays the entire closing timeline.

No. It simply means you agree with the loan estimate, not that you are legally obligated to purchase the property.

Make sure the interest rate, monthly payment, and closing costs match what you discussed with your loan officer.

📝 Quick Checklist

| Checklist | Checklist |

|---|---|

| Document Upload | Have you uploaded the requested income and asset documents in PDF format? |

| Initial LE Confirmation ITP Signing | Have you reviewed the interest rate and fees listed in the Initial LE? |

| ITP Signing | Have you completed the E-signature of the ITP (the faster, the better!) |

![Things to Check When Your Closing Disclosure and LE Don’t Match [Mortgage Guider Ep. 6]](https://blog.loaning.ai/en/wp-content/uploads/2026/01/6-350x250.jpg)

![Revised LE & Rate Lock: What to Do and When [Mortgage Guide Ep. 5]](https://blog.loaning.ai/en/wp-content/uploads/2026/01/5-350x250.jpg)

![The Hidden Truth Behind U.S. Mortgage Underwriting: Why Do Approvals Get Delayed? [Mortgage Guide Ep. 4]](https://blog.loaning.ai/en/wp-content/uploads/2026/01/4-350x250.jpg)