When entering the U.S. real estate market, you’ll encounter many unfamiliar terms. If you’re planning to purchase a high-priced property, one concept you must understand is the Jumbo Loan.

As the name suggests, a Jumbo Loan refers to a mortgage that exceeds standard lending limits. However, it’s not simply about borrowing a large amount — it’s defined by specific federal loan limits.

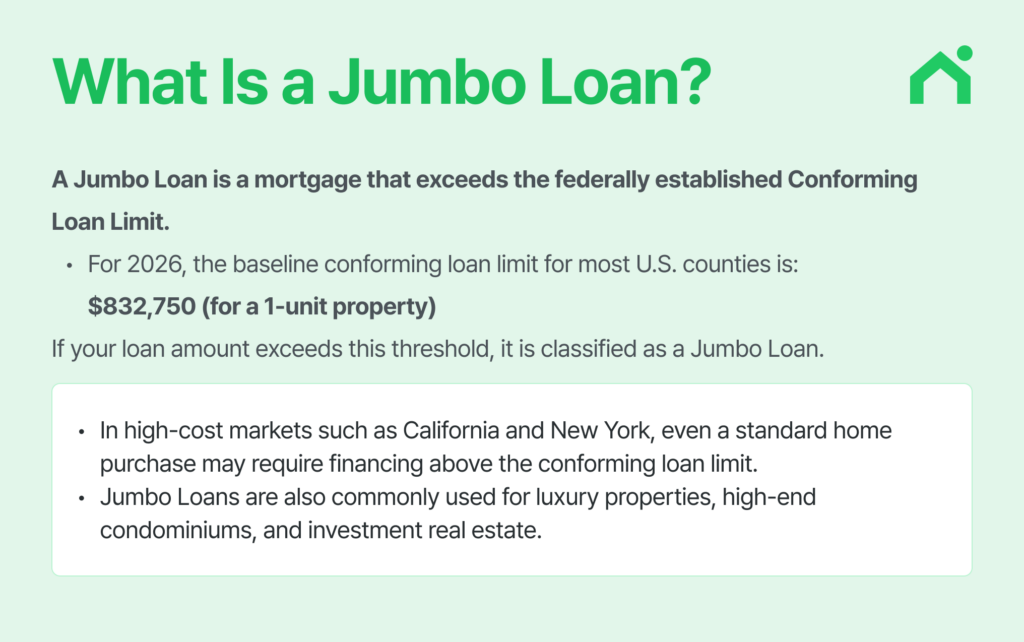

What Is a Jumbo Loan?

A Jumbo Loan is a mortgage that exceeds the federally established Conforming Loan Limit.

For 2026, the baseline conforming loan limit for most U.S. counties is:

$832,750 (for a 1-unit property)

If your loan amount exceeds this threshold, it is classified as a Jumbo Loan.

In simple terms, if a property’s price requires borrowing more than the conforming limit, you’ll need a Jumbo Loan instead of a conventional conforming mortgage.

Jumbo Loan vs. Conforming Loan

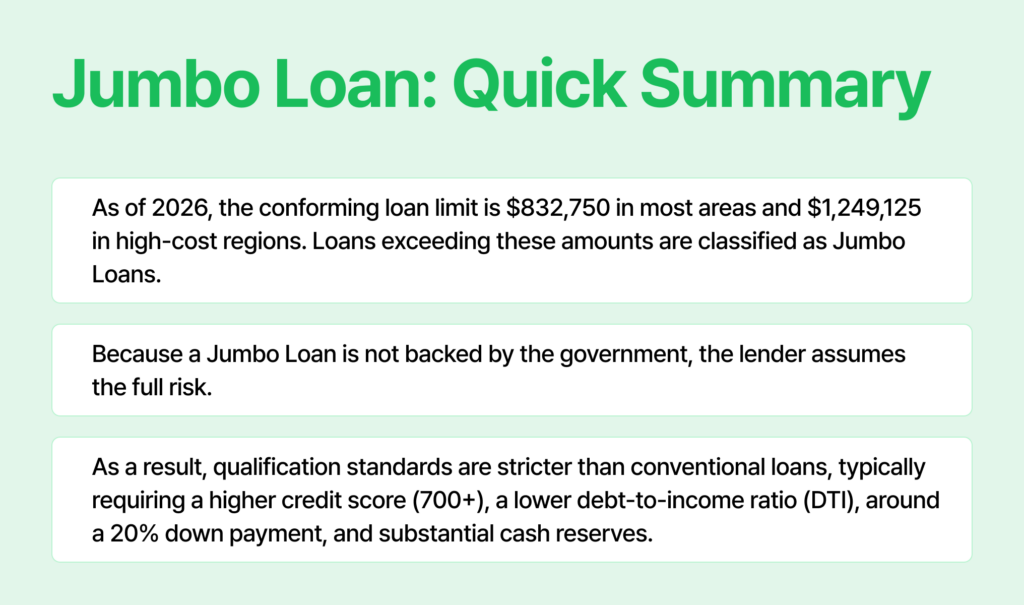

Unlike conforming loans, which are backed by Fannie Mae or Freddie Mac, a Jumbo Loan is not government-sponsored. The lender assumes the full risk, which results in stricter qualification standards.

| Criteria | Conforming Loan | Jumbo Loan |

|---|---|---|

| Credit Score | 620+ | Typically 700+ |

| Down Payment | As low as 3% | 10–20% or higher recommended |

| DTI Ratio | Up to 45–50% | Typically 43% or lower |

| Cash Reserves | 0–6 months | 6–18 months of payments |

| Government Backing | Yes | No |

In general, Jumbo Loans are designed for higher-income borrowers with strong credit and substantial assets.

Are Jumbo Loan Interest Rates Higher?

Historically, Jumbo Loan rates were higher than conforming loans. However, that’s not always the case today.

Reason 1: Jumbo borrowers typically have strong credit profiles and stable income, making them lower-risk clients.

Reason 2: Banks often view Jumbo borrowers as long-term private banking or wealth management clients, leading to competitive rate offerings.

Pros and Cons of a Jumbo Loan

👍 Advantages

- Enables purchase of high-value properties

- Allows financing large loan amounts under a single mortgage

- Competitive rates for qualified borrowers

👎 Disadvantages

- More complex and lengthy approval process

- Stricter credit, income, and asset requirements

- Larger down payment needed

2026 Jumbo Loan Limits Explained

Each year, the Federal Housing Finance Agency (FHFA) adjusts conforming loan limits based on housing price trends.

For 2026:

Baseline Limit (Most U.S. Counties)

- $832,750 (1-unit property)

Loans above this amount are considered Jumbo Loans.

High-Cost Areas

In designated high-cost areas (e.g., parts of California, New York, Florida), the limit increases to:

- $1,249,125

Any mortgage amount that exceeds the applicable conforming loan limit is classified as a Jumbo Loan.

The conforming loan limits also increase based on property type, with higher limits available for multi-unit properties such as duplexes (2 units) and triplexes (3 units).

2026 conforming loan limits

| Property Type | Low-cost areas | High-cost areas | Hawaii (high-cost) |

|---|---|---|---|

| 1 unit | $832,750 | $1,249,125 | $1,299,500 |

| 2 units | $1,066,250 | $1,599,375 | $1,633,600 |

| 3 units | $1,288,800 | $1,933,200 | $2,010,950 |

| 4 units | $1,601,750 | $2,402,625 | $2,499,100 |

Frequently Asked Questions (FAQ)

Q1: If my down payment is less than 20%, do I need to pay PMI (Private Mortgage Insurance) on a jumbo loan?

A: Generally, jumbo loans do not require PMI even with a down payment below 20%. PMI is primarily associated with conforming loans when the down payment is less than 20%. In many cases, PMI products are simply not available in the jumbo loan market.

Instead, lenders manage risk through other means. Most require a substantial down payment—typically 10% to 20% or more—as a baseline condition. If certain specialty programs offer jumbo loans with less than 20% down, they may offset the risk by charging a higher interest rate rather than requiring PMI.

Q2: Can I use a jumbo loan to buy a second home or investment property?

A: Yes, you can. Many lenders offer jumbo loan products for purchasing second homes or investment properties, not just primary residences.

However, the requirements are significantly stricter than for a primary residence. Generally, you can expect to need a higher credit score (e.g., 720 or 760+), a larger down payment (up to 40% for some investment properties), and greater cash reserves.

Q3: Are closing costs for jumbo loans much higher than for conventional loans?

A: Yes, they are. The absolute amount of closing costs is typically much higher for jumbo loans. There are two main reasons:

Fee Structure: Some closing costs (such as origination fees) are calculated as a percentage of the loan amount. Since jumbo loans involve larger principal amounts, these costs naturally increase in absolute terms.

Additional Requirements: Lenders may require extra procedures to reduce risk. A common example is a dual appraisal, where two independent appraisers evaluate the property’s value. This further increases closing costs.

Q4: Can jumbo loans be refinanced? What are the conditions?

A: Yes, jumbo loans can be refinanced. Refinancing allows you to secure a lower interest rate, adjust your loan term, or cash out home equity.

However, refinancing underwriting is just as rigorous as the original loan approval. Typical requirements include:

- High Credit Score: Usually 680+; for 15-year fixed or ARM products, 740+ may be required.

- Low DTI (Debt-to-Income Ratio): 45% or lower; some lenders prefer 36% or below.

- Sufficient Home Equity: Often, you must retain at least 20% equity in the home after refinancing.

- Substantial Cash Reserves: Lenders typically want proof that you can cover 6 to 12 months’ worth of payments in cash reserves after the refinance.

Q5: Are there jumbo loan options other than 30-year fixed rates?

A: Yes, there are various options. While 30-year and 15-year fixed-rate loans are most common, many lenders also offer Adjustable-Rate Mortgages (ARMs).

ARM products are typically labeled as ‘5/6m ARM’ or ‘7/6m ARM’. This means the interest rate is fixed for the first 5 or 7 years, then adjusts every 6 months based on market rates. The initial fixed rate is often lower than a traditional fixed-rate loan, which can benefit buyers who don’t plan to stay in the home long-term.

Some lenders also offer interest-only options, where you pay only interest for the first few years.

Q6: How is a ‘Super Conforming Loan’ different from a jumbo loan?

A: A Super Conforming Loan sits between a standard conforming loan and a jumbo loan. In certain high-cost areas of the U.S. where home prices are especially high, higher conforming loan limits apply beyond the national baseline.

- Super Conforming Loan: Exceeds the national baseline limit but stays within the high-cost area’s ceiling. It is still classified as a conforming loan and can be backed by government-sponsored enterprises (GSEs).

- Jumbo Loan: Exceeds even the high-cost area’s ceiling.

Because Super Conforming Loans remain conforming, they tend to have less stringent qualification requirements (credit score, down payment, etc.) and more competitive interest rates than jumbo loans—making them a more favorable option for buyers in high-cost areas.

Quick Summary

Find the Right Mortgage Option for You

Whether a Jumbo Loan fits your profile depends on your income, credit, assets, and long-term financial goals.

Use Loaning.ai to explore customized mortgage scenarios and determine whether a Jumbo Loan or another loan structure best fits your situation.