Buying a home in the United States almost always involves one key financial concept: a mortgage. Understanding how a U.S. mortgage works is essential before using a U.S. bank mortgage calculator. It allows buyers to purchase a home by paying over time rather than upfront. More importantly, it is not simply “a loan for a house” — it is a structured financial contract backed by the property itself.

In this article, we will focus on how a U.S. mortgage actually works, and what you should understand before using a u.s. bank mortgage calculator to estimate your monthly payment.

What Is a U.S. Mortgage?

A U.S. mortgage is an agreement in which a lender provides funds to purchase a home, and the borrower repays that amount over an extended period.

Typically:

- The buyer makes a down payment.

- The remaining balance is financed through a mortgage loan.

Once the loan closes:

- Ownership of the home transfers to the buyer.

- The lender places a lien on the property as security.

This means the home legally belongs to the buyer, but the lender holds a secured interest in the property until the loan is fully repaid.

How Does a U.S. Mortgage Work?

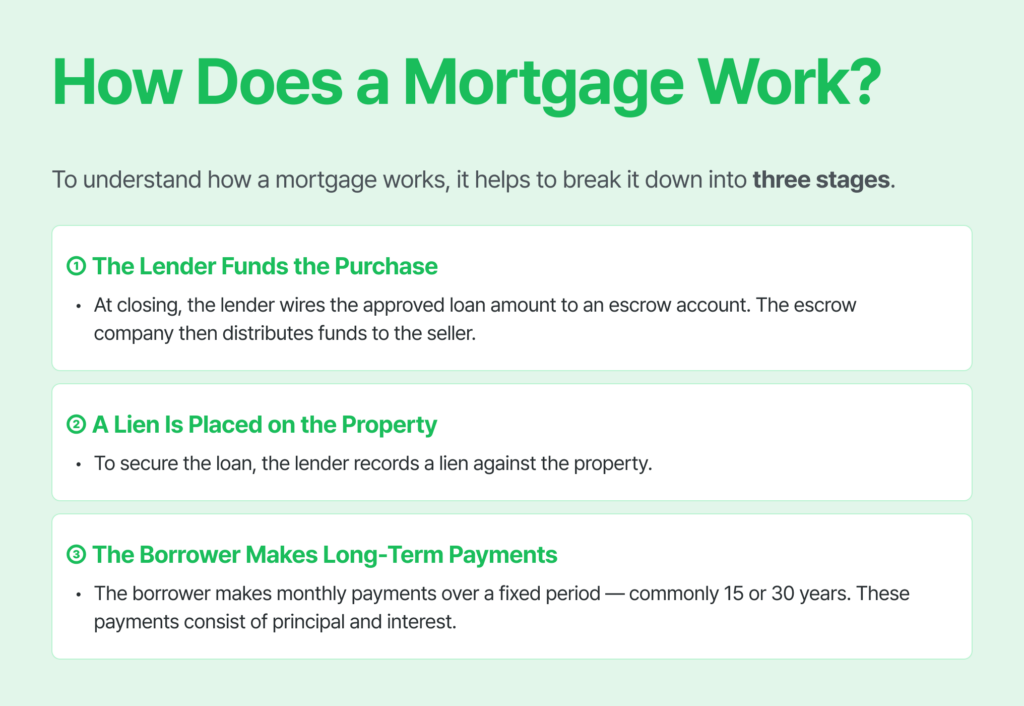

To understand how a U.S. mortgage works in practice, it helps to break it down into three stages.

① The Lender Funds the Purchase

At closing, the lender wires the approved loan amount to an escrow account. The escrow company then distributes funds to the seller.

This is how the purchase is completed even though the buyer did not pay the full price in cash.

② A Lien Is Placed on the Property

To secure the loan, the lender records a lien against the property.

If the borrower stops making payments, the lender has the legal right to pursue foreclosure and recover the remaining loan balance through sale of the home.

③ The Borrower Makes Long-Term Payments

The borrower makes monthly payments over a fixed period — commonly 15 or 30 years.

These payments consist of:

- Principal

- Interest

Understanding how these two components work is essential before estimating payments using a u.s. bank mortgage calculator.

How Are Monthly Mortgage Payments Structured?

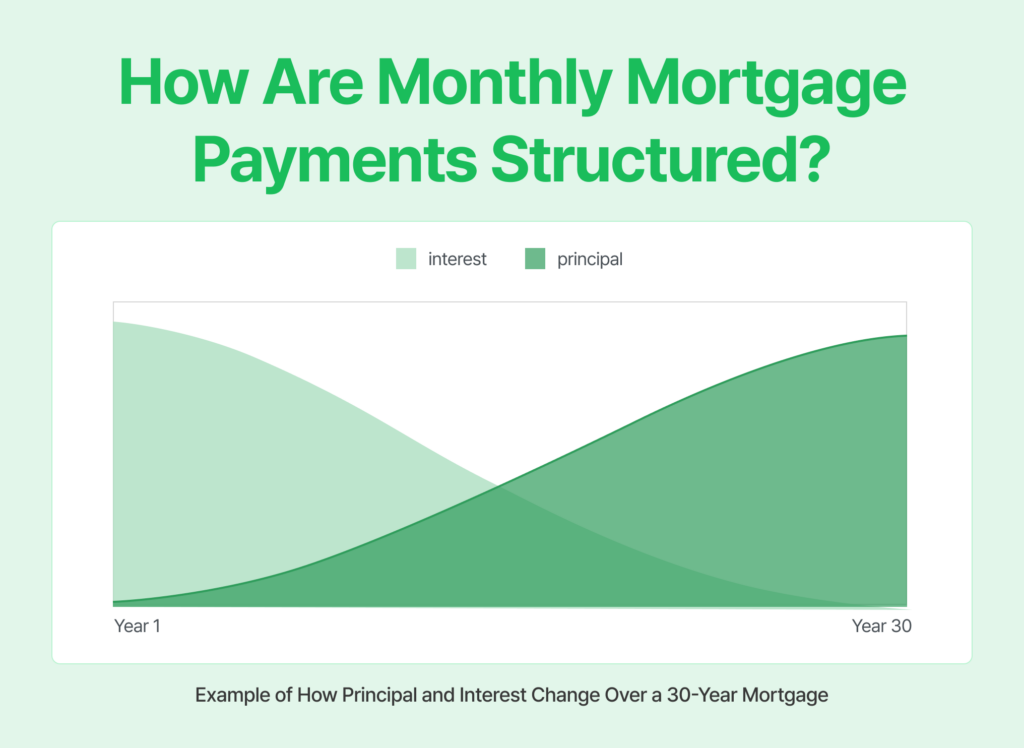

Most U.S. mortgages are fully amortized.

This means:

- The monthly payment amount is generally consistent.

- The proportion of principal and interest changes over time.

Early in the loan:

- A larger portion of the payment goes toward interest.

Later in the loan:

- A larger portion goes toward principal.

Because interest is calculated based on the remaining loan balance, early payments reduce principal slowly. This is why the loan balance does not seem to drop significantly at the beginning.

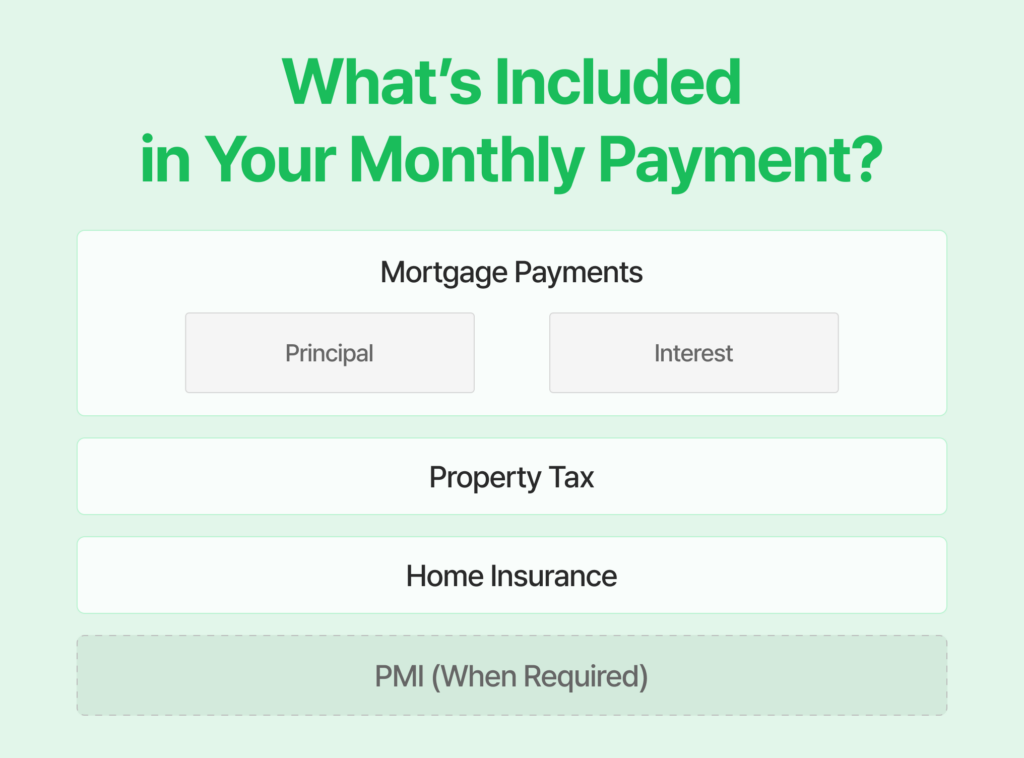

What May Be Included in the Total Monthly Payment?

The “loan payment” often refers to principal and interest only.

However, the total monthly amount withdrawn from your bank account may be higher.

In many U.S. mortgages, additional items are included:

- Property Tax

- Homeowners Insurance

These costs are often managed through an escrow account.

The lender collects a portion of these expenses monthly and pays them on your behalf when they are due.

If your down payment is less than 20%, you may also be required to pay:

- PMI (Private Mortgage Insurance)

PMI is added to your total monthly payment and protects the lender — not the borrower — in case of default.

For accurate budgeting, a U.S. bank mortgage calculator should factor in not only principal and interest, but also taxes, insurance, and potential PMI.

What Happens as You Pay Off the Mortgage?

As you make payments, the principal balance decreases.

This builds equity — your ownership stake in the property.

When the mortgage is fully repaid:

- The lien is removed.

- The property becomes your free-and-clear asset.

This is why a U.S. mortgage is often viewed not just as debt, but as a long-term wealth-building structure.

U.S. Mortgage at a Glance

A U.S. mortgage is:

- A long-term loan secured by real estate

- A contract where the lender funds part of the purchase price

- A structure where the borrower repays principal and interest over time

- A system that gradually builds home equity

In simple terms, buying a home with a mortgage means entering a structured financial agreement within the broader U.S. lending system.

Understanding Your Mortgage Before Calculating Payments

Understanding a U.S. mortgage is not just about knowing the interest rate.

It means understanding:

- How amortization works

- What makes up your true monthly payment

- How escrow and PMI affect overall costs

- How equity builds over time

Before relying on any U.S. bank mortgage calculator, make sure you understand the numbers you are entering — and what they actually represent.

Check current rates and estimate your monthly payment at Loaning.ai.