When buying a home in the United States, many people focus mainly on the down payment and the monthly mortgage payment. However, another cost may appear during the homebuying process: private mortgage insurance (PMI). Because of this, many buyers begin asking what PMI in mortgage is and how it can affect their overall home-buying costs.

PMI is an additional expense that can apply when a borrower makes a relatively small down payment. Understanding what PMI is, why it exists, and how it can be avoided is important for anyone planning to buy a home.

In this guide, we will explain what PMI in mortgage is, why lenders require it, how much it typically costs, and strategies that may help you avoid it.

What Is PMI in Mortgage?

PMI stands for Private Mortgage Insurance, a type of insurance that may be required when purchasing a home with a mortgage loan.

Unlike homeowners insurance, PMI does not protect the homebuyer. Instead, it protects the lender. If the borrower fails to repay the mortgage, PMI helps cover part of the lender’s potential loss.

In most cases, PMI is required when the down payment is less than 20% of the home price. When a borrower contributes a smaller down payment, lenders consider the loan riskier, which is why PMI may be required.

Why Do Lenders Require PMI?

The main purpose of PMI is to reduce lending risk.

When buyers put down a smaller down payment, they have less equity in the home at the start of the loan. From a lender’s perspective, this increases the financial risk if the borrower stops making payments.

PMI helps offset that risk.

However, PMI is not always a disadvantage for homebuyers. Because PMI exists, buyers may be able to purchase a home without waiting years to save a full 20% down payment.

How Much Does PMI Cost in a Mortgage?

The cost of PMI varies depending on several factors, including:

- Down payment amount

- Loan size

- Credit score

In many cases, PMI costs about 0.3% to 1% of the loan amount annually.

This cost is typically added to the monthly mortgage payment.

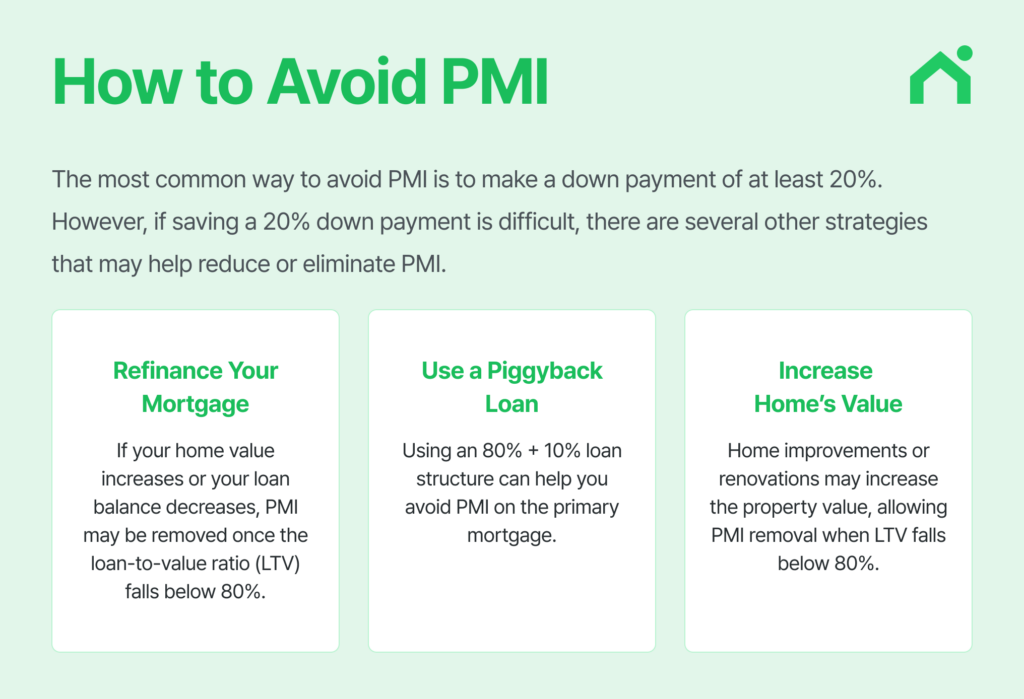

How to Avoid PMI

The most common way to avoid PMI is to make a down payment of at least 20%. In conventional mortgage loans, PMI is usually not required once the down payment reaches this level.

However, if saving a 20% down payment is difficult, there are several other strategies that may help reduce or eliminate PMI.

1. Refinance Your Mortgage

If your home value increases or your loan balance decreases, refinancing may allow you to remove PMI.

When refinancing into a new loan, PMI may no longer be required if the new loan balance is below 80% of the home’s value (LTV 80%).

Additionally, if mortgage interest rates have decreased since you first obtained your loan, refinancing may help you secure better loan terms. Keep in mind that refinancing typically involves closing costs.

2. Use a Piggyback Loan

A piggyback loan structure uses two loans instead of one mortgage.

Example structure:

- First mortgage: 80%

- Second loan: 10%

- Down payment: 10%

Because the primary mortgage covers only 80% of the home’s value, this structure may help borrowers avoid PMI.

3. Increase Your Home’s Value

Improving or renovating your home can increase its market value.

If the home value rises enough that your loan balance becomes less than 80% of the property value, you may be able to request PMI removal. In this way, increasing home value may help eliminate PMI sooner.

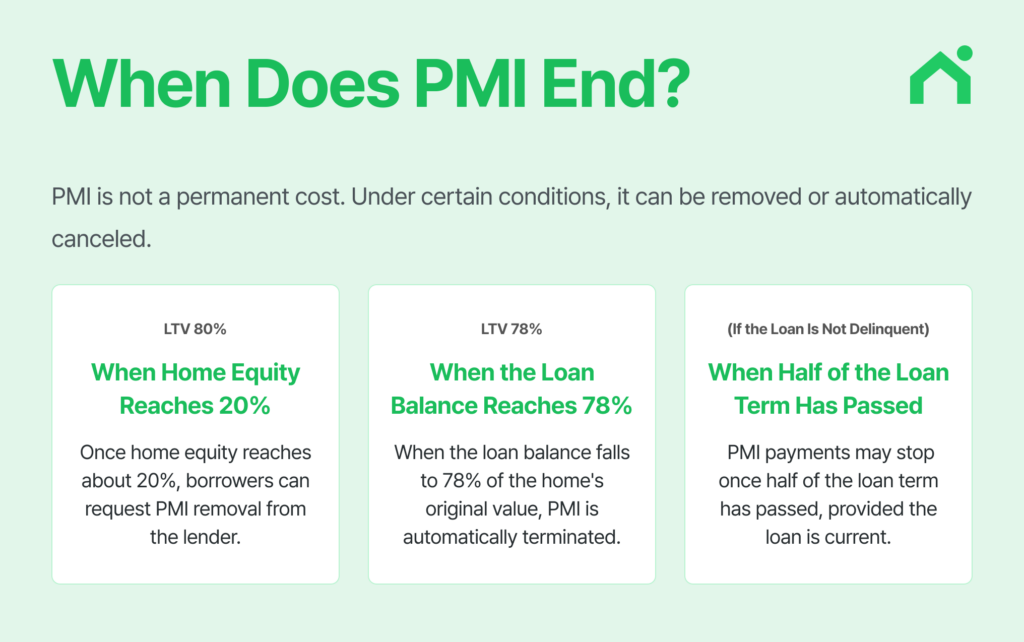

When Does Private Mortgage Insurance (PMI) End?

PMI is not a permanent cost. Under certain conditions, it can be removed or automatically canceled.

Typically, borrowers can request PMI removal once they reach about 20% equity in the home, meaning the loan balance falls to about 80% of the home’s original value (LTV 80%).

Under the Homeowners Protection Act, PMI must automatically terminate when the loan balance reaches 78% of the home’s original value, as long as the mortgage payments are current.

In addition, PMI may also end when half of the loan term has passed, even if the 78% loan-to-value threshold has not yet been reached.

As you continue paying down your mortgage and building equity, PMI will eventually no longer be required.

Understanding PMI Helps You Plan Your Home Purchase

PMI may seem like just another cost, but it plays an important role in the overall strategy of buying a home.

In some cases, it may make sense to wait and save for a larger down payment. In other situations, paying PMI temporarily may allow buyers to purchase a home sooner.

For many buyers, understanding what PMI in mortgage is, how it works, and when it may be required can help them make a more informed decision when planning their home purchase.

👉 Check current mortgage rates and estimated monthly payments with Loaning.ai.