TurboHome Review: Key Takeaways

- The flat-fee model charges a fixed service fee regardless of the home’s purchase price, which may offer greater savings when buying a higher-priced property.

- The potential savings may be used strategically toward closing costs, discount points, or eligible temporary buydown expenses, such as a 2-1 buydown.

- Eligibility and permitted uses may vary depending on state regulations, lender policies, loan program requirements, and the terms of the transaction, so buyers should confirm the details in advance.

Buyer rebate platforms have been gaining significant attention in the U.S. housing market. According to transaction data published by TurboHome, buyers received an average rebate of approximately $25,000.

However, because the idea of charging a flat fee and returning the remaining commission to the buyer is still unfamiliar to many people, it’s no surprise that prospective homebuyers often wonder whether the service is legitimate and search for real TurboHome reviews before making a decision.

The reason TurboHome is able to offer substantial buyer rebates is its flat-fee pricing model. Instead of charging a commission based on the home’s purchase price, TurboHome charges a fixed service fee, allowing eligible buyers to receive part of the remaining buyer agent compensation as a rebate.

In this guide, we’ll explain how TurboHome’s business model works, how buyer rebates are calculated, and what homebuyers should know before using the service. 🚀

.

TurboHome Review: Understanding the Flat-Fee Model

Traditional real estate brokerage commissions are often calculated as a fixed percentage of the home’s price. In other words, the higher the home’s price, the higher the commission paid to the agent.

In contrast, TurboHome uses a flat-fee structure, charging a fixed amount upon completion of the transaction rather than a commission proportional to the home’s price.

Since the commission does not vary in proportion to the sale price, the potential for commission savings is greater in areas with higher home prices.

However, the scope of services provided may vary depending on the agent’s contract, so you should carefully review the included services in advance.

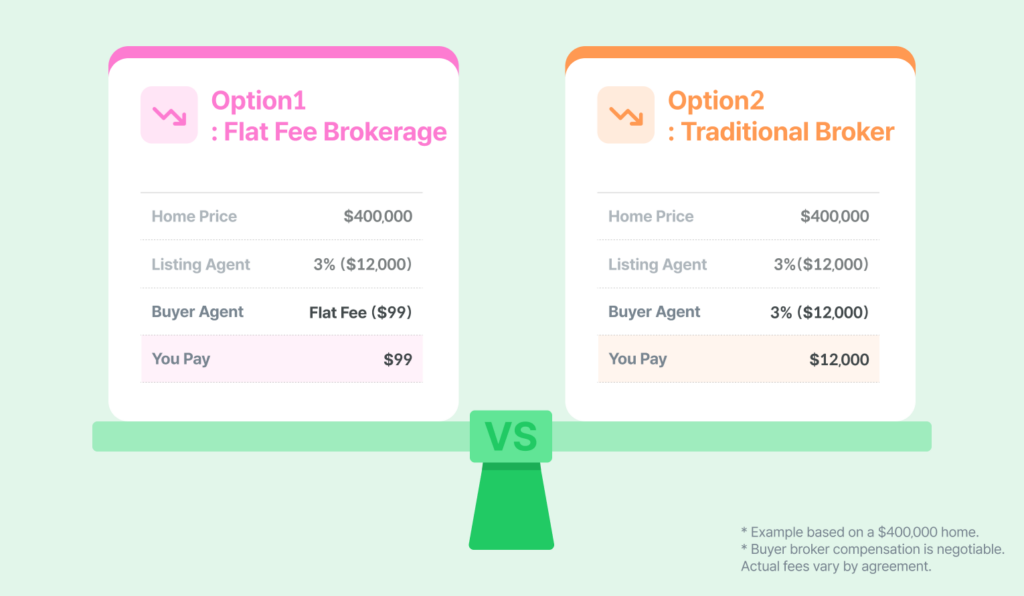

If the seller pays a $22,000 commission to the buyer’s agent and TurboHome receives a $10,000 flat fee, the difference—approximately $12,000—could be used as a rebate fund.

However, the actual rebate amount varies depending on the home’s price, contract terms, local regulations, and the commission offered by the seller.

.

How are actual rebates calculated on TurboHome?

To help illustrate this, let’s assume that the seller has set aside $22,000 as compensation for the buyer’s agent.

If TurboHome receives a flat fee of $10,000 for that transaction, the remaining amount, based on a simple calculation, is as follows:

$22,000 − $10,000 = $12,000

In this case, the difference—approximately $12,000—may be offered to the buyer as a buyer rebate.

.

How can a buyer rebate be used?

A buyer rebate isn’t simply an amount returned in cash after a transaction is completed; depending on the loan and transaction terms, it can be used in the following ways.

.

2-1 Buydown Mortgage Structure and Usage

Many buyers consider a 2-1 buydown mortgage to ease the initial interest rate burden.

This is a loan structure where the interest rate is 2% lower in the first year, 1% lower in the second year, and returns to the originally agreed-upon note rate starting in the third year.

For example, if the final agreed-upon interest rate is 6.5%, it is applied as follows:

- First year: Monthly payments calculated based on a 4.5% interest rate

- Second year: Monthly payments calculated based on a 5.5% interest rate

- From the third year onward: Monthly payments calculated based on the original note rate of 6.5%

This strategy can help significantly reduce the burden of monthly payments during the first one to two years.

It is a practical option worth considering, especially for buyers who expect their income to increase in the future due to a job change or promotion, or who are considering refinancing in anticipation of future interest rate declines.

However, since future interest rate declines and refinancing are not guaranteed, you should assess whether you can afford the original payment amount starting in the third year. You must also confirm with your lender in advance whether the rebate can be fully applied toward the buydown cost.

.

If I consider refinancing in the future, what will happen to the escrow account?

2-1 A buydown may involve setting aside a certain amount in an escrow account to cover the difference in monthly payments during the first 1 to 2 years.

If market interest rates drop during this period and you refinance early, you must confirm in advance with the lender exactly how any unused balance in the escrow or buydown account will be handled.

Depending on the product structure and the lender’s policies, this remaining amount may be applied toward the principal balance of the new loan or adjusted as a credit during the settlement process; it cannot be assumed that the customer will automatically be able to recover it as cash.

.

TurboHome Review: Frequently Asked Questions (FAQ)

.

With Loaning.ai

If you’re considering a flat-fee real estate option like TurboHome, it’s important to see how the savings might affect your actual monthly payments and closing costs.

Use Loaning.ai, a direct lender, to clearly compare estimated monthly payments, various interest rate options, and the possibility of a 2-1 buydown. 🏡💚

.

This content is provided for informational purposes only and does not constitute legal, tax, real estate, or lending advice. TurboHome’s service structure and disclosed transaction examples are subject to change depending on the timing and terms of the transaction. The availability, actual amount, and usage of the Buyer Rebate may vary depending on state laws, brokerage agreements, seller incentives, loan programs, and lender approval criteria. Please consult a qualified professional to verify your individual circumstances before making any decisions regarding a home purchase or loan.

.